- English (UK)

March 2026 UK Inflation: The Energy Shock Starts To Arrive

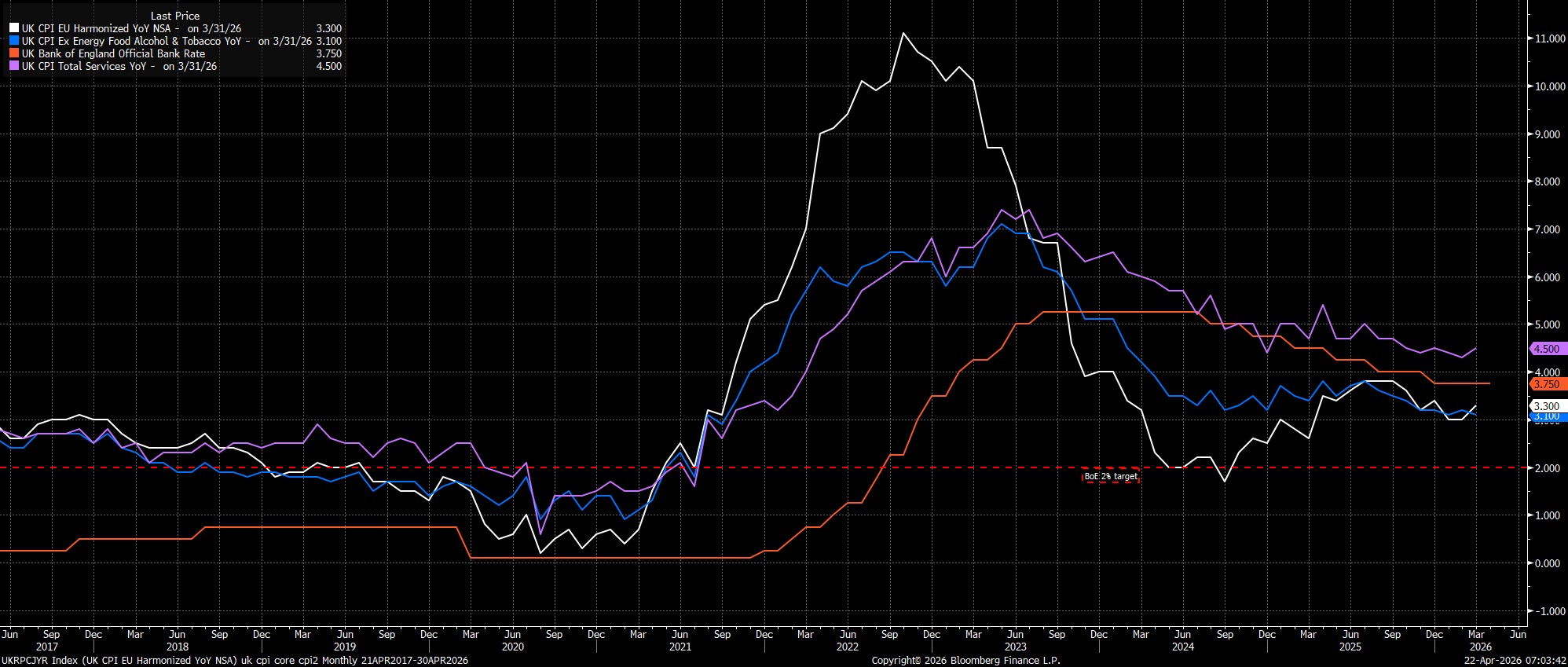

Headline CPI rose 3.3% YoY last month, the fastest pace since last December, with almost all of the uptick in inflation stemming from higher energy prices, most notably feeding through in the form of a surge in the prices of both motor fuel, and of heating oil, with the former rising at its fastest pace in more than three years. Of course, in contrast to other DM economies, the impact on consumer gas and electricity prices has not yet been felt, but will feed into the data from July, once the Ofgem price cap has been re-set. In any case, the headline print was roughly in line with the MPC's expectations, after the March statement noted an expectation that headline inflation would print "close to" 3.5% YoY last month.

Amid the energy-induced jump in headline inflation, metrics of underlying price pressures were something of a mixed bag. Core CPI, for instance, rose 3.1% YoY, equalling the low seen in January, while services CPI ticked up to 4.5%% YoY, a YTD high, and a fair chunk above the Bank's 4.1% YoY forecast.

Zooming out, this morning's data seems unlikely to impact the near-term Bank of England policy outlook especially much. While the data reflects some of the initial, first-round effects of the energy price shock, it is the second-round effects of higher energy prices to which policymakers are likely to pay much more attention, and which will determine any policy response that may be delivered.

On this front, the potential for significant second-round effects, and subsequently for higher energy prices to spill-over into broader price pressures, seems relatively limited, owing not only to the substantial margin of slack that continues to emerge in the labour market, and the limited pricing power that corporates currently possess, but also in light of inflation expectations remaining well-anchored for the time being.

With that in mind, the MPC are likely to retain their 'wait and see' approach for the time being, holding Bank Rate steady at the April confab, with the already-restrictive policy stance leaving little need to tighten policy further at the current juncture.

In fact, given that a short-lived 'hump' in headline CPI, as opposed to longer-lasting price pressures, is the base case as to how higher energy prices will impact the inflation outlook, there remains a path to one, or two, rate cuts still being delivered in the second half of the year. Said cuts, however, would require the MPC to have obtained adequate confidence in price pressures proving temporary in nature, with such confidence in turn permitting a modest degree of loosening in order to cushion against the negative demand shock that is likely to eventuate from higher energy costs.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.